Current State of AI Apps

Vertical AI? AI Native Apps? The Current State - All Things Venture #102

I recently wrote an essay on the current state of VC, and it was well received so I wanted to write about another undercurrent within the VC ecosystem which is the rise of Vertical AI. What is Vertical AI you may ask? Great question! To put it bluntly, it’s just marketing.

It’s clever, opportunistic marketing but marketing nonetheless. Vertical AI is a broad, amorphous category that is being applied to any software company that has now remotely mentioned their usage of AI in any part of their business. In its best, most ambitious form, Vertical AI is touting laudatory intentions such as, “our goal is to create a magical tool with the aim of writing all of the world's software.”

In it’s worst, most ambiguous, marketing mumbo-jumbo, say something without really saying anything form, Vertical AI companies say things like this, “AI isn’t next, it’s now. Harness it with Jasper to transform your creative capability, better connect with your customers, and secure your competitive advantage.”

One sounds like their genuine ambition is to change the world, and the other sounds like an A/B test to drive next month’s ARR target.

When most people talk about Vertical AI, I think they really are just talking about the next generation of the “application software” category.

In more detail, I would define Vertical AI companies as companies that, without leveraging one of the foundational LLMs and/or their own ML based models, would not be compelling opportunities for VC financing AND Vertical AI companies are distinctly focused on specific industries or professions (i.e Legal Services, Financial Services, Transportation & Logistics, etc.)

There are different types of Vertical AI companies coming to market. There are 5 main buckets of companies that I am consistently seeing. These types of Vertical AI companies are:

Model Wrappers: Just ping an API end point, and effectively act as distribution. Extremely light workflow complexity, low on the sniff test for defensibility (i.e Jasper)

Mesh Assistants: AI acts as an omnipresent assistant that takes unstructured data, often in the form of meeting transcripts, from across the org and places it into structured outputs such as Slack, Salesforce or ERPs. Generally focused on automating administrative tasks (i.e Inputting call notes from a sales call)

Co-Pilots: Domain specific and heavily focused on chat interfaces, do some level of RAG or combine additional data to provide higher fidelity responses. Often embedded directly into another workflow where the work is done (i.e GitHub Copilot, Robin AI), Stronger focus on relying on the model to generate net new data and complete more strategic tasks than Mesh Assistants

Operating Systems: Combine co-pilot functionality with additional workflow - extends out into collaboration, multiplayer tooling, and the goal for the business is to be the default place where work is done (i.e Harvey AI, Rogo, Cursor). Will steer more into enterprise use cases for large organizations. Heavy focus on driving incremental productivity for IC

Service Companies: Exactly how it sounds, AI is doing the work that you asked for. These are the least common companies coming to market today.

Overwhelmingly, VC funding is going to Co-Pilots and Operating Systems. The industry believes that these companies are the next generation of fund returners, but only time will tell if that belief will turn into reality. So if VC left and right, old and new, are betting the house on AI. What is actually going on in the market?

From my vantage point, I’m seeing a few things going on:

Entrepreneurs sense the opportunity. The % of YC companies that are categorized as AI grew +500% in a 4 year period. More than 1 in 3 YC companies in the latest batch are focused on AI. Up from 1 in 15 in 2020

Of this most recent batch, nearly ~70% of companies in this YC cohort can be classified as OS or Co-Pilot type businesses

While industry focus is diffuse in nature 3 clear focus areas emerge 1) Developer Tools 2) Horizontal B2B Software (would not classify as Vertical AI by my definition but including as a reference point) 3) Healthcare

Taking a step back to look at overall VC investment in 2024, the foundational model layer continues to dwarf Vertical AI. $13bn has been invested in the likes of Anthropic, xAI, Mistral, Cohere, and the H Company. Whereas $5.5bn has been invested in companies like Andruil, Xaira, Figure AI, AlphaSense, Poolside and more

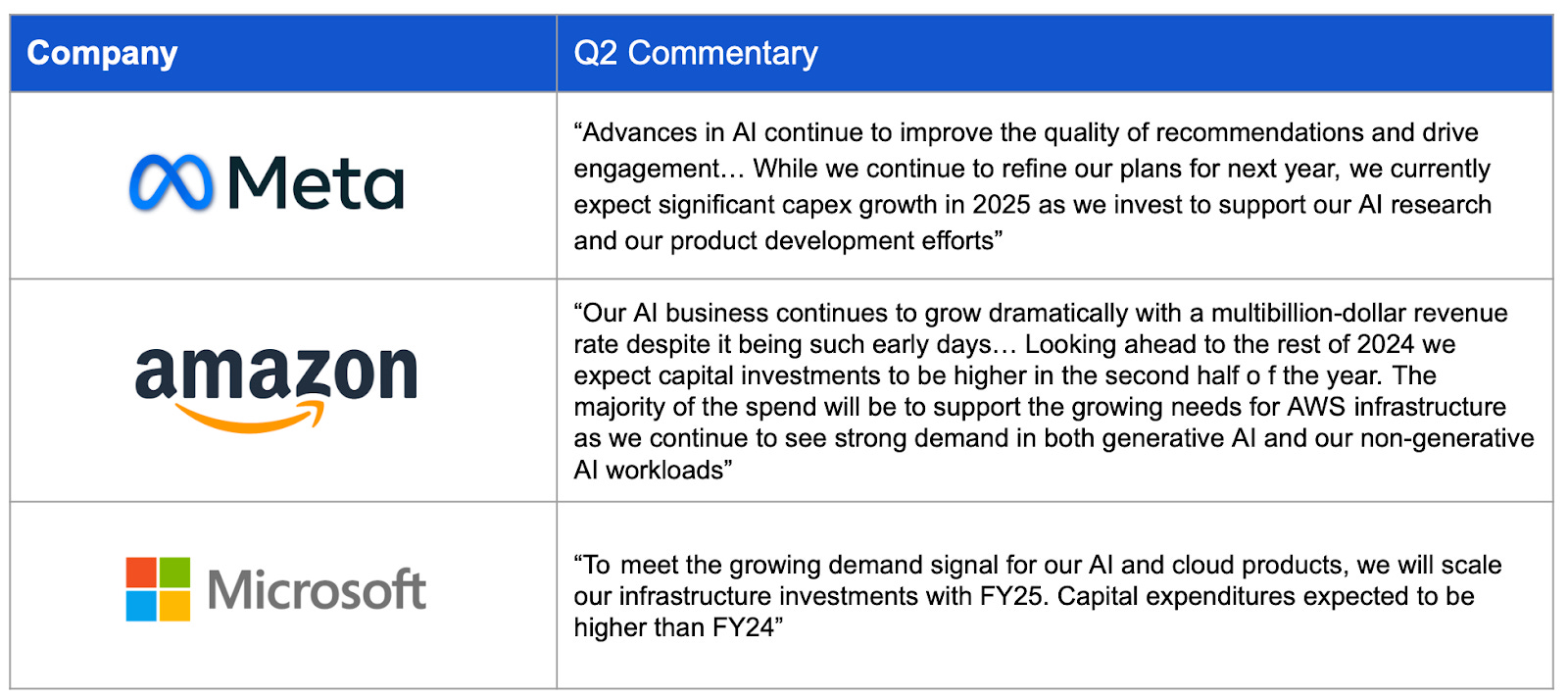

Public market participants are signaling their commitment to, interest in, and success from the AI tailwind

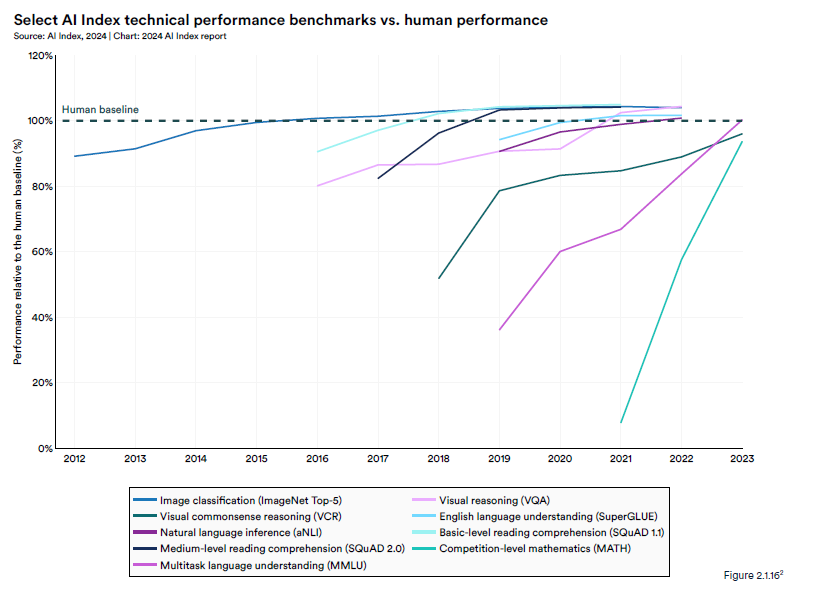

And the research community continues to publish data showing the efficacy of generative AI

Further, the research community is also showing

Agents are shown to be cheaper than humans in certain software engineering/IT related tasks

Agents are demonstrating the ability to generate and document scientific experiments autonomously

AI can be used generate human level voice cloning

The current course and speed of the industry tells the following:

There is tremendous investment (that is seeking a return) in both public & private markets

A new generation of entrepreneurs is energized by the hype cycle and capital flows - these entrepreneurs are all seeking to create and capture durable economic value

The OS & Co-Pilot businesses models are emerging as more durable relative to the model wrappers

The underlying foundational models continue to improve and be applied in novel ways

All of the above tells us that for the foreseeable future, call it another year minimum, we are going to see even more entrepreneurs enter the vertical AI fray. Those entrepreneurs will take inspiration from their peers and the most hyped/media covered AI businesses of late, which will be Co-Pilot & OS type businesses. These new entrepreneurs will research what is and isn’t working (and also recruit from these companies) and tweak things to attack their own hypothesis.

In addition, by the end of 2025 or early 2026 we’ll probably have a version of GPT-5 , so we can assume that the capabilities of all of these hypothetical new entrants will be leveled up as well.

Where does that leave us?

In the very simplest terms, we’ll have an oversupply of entrepreneurs focused on similar sets of problems. Early stage VCs will happily invest in these businesses/founders at inception because the narrative makes sense, it’s what LPs pay us to do, and the initial trajectory out of the gate will be sufficient to get past a Seed or Series A round.

The real problems will start at the Growth stages when there are 3 - 5 companies all with similar value props, unit economics, and revenue growth. They’ll viciously compete and undercut each other on price because in most cases, they’ll be competing at parity. They’ll use the same recruiting firms, recruit from the same talent pools, and offer similar compensation packages. They’ll have similar(ish) visions, have similar GTM motions, and have parallel product roadmaps. Multi-stage firms will look to anoint “winners” pre-maturely because they will only be able to return multi-billion dollar fund sizes if they have significant exposure to $50bn + outcomes. This is where the current state of Vertical AI is headed. Buyer (and entrepreneur) beware.

Knowing all of this, and using it as a proxy for the current state, it reaffirms my belief that the most exciting place an entrepreneur can be focused right now is on building a service business.

In contrast to where the current state of Vertical AI is headed, the idea of selling services, and backing entrepreneurs that are focused on selling services, is attractive to me for three reasons:

The VC industry doesn’t widely understand how to underwrite a service focused firm (it’s anathema to invest in something sub 80% gross margins)

Because of this lack of understanding, It’s less competitive

Because these end markets are less competitive, it’s more likely that any given business can truly reach escape velocity (in the near term)

Notwithstanding my own career choices, competition is the bane of my existence as an investor. Why compete and sell against 20 other people who are trying to reinvent the ERP when you could be the N of 1 company who helps auto repair shops find incremental revenue? Why consider creating an incremental LLM Ops platform when there’s been $2bn of Gen AI related sales captured by Accenture in a single year?

Need more reasons to see the potential for services being automated via software? Mark Zuckerberg himself is charting a path toward purely selling services, “over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we’re going to do the rest for them. We’re going to get there incrementally over time, but I think this is going to be a very big deal.”

That is the founder of $1.35 trillion dollar, generational company; who has one of the best vantage points on the current state of AI, publicly saying that the future state of his business will have the ability to go to a Nike, or a P&G, or a Target and say, “Oh by the way - you know that $100M of creative and professional services related talent you spend each year? Yeah. Not the actual ad budgets but like the people behind that? We can take care of all of that for you now too.”

What people want today, and what they will continue to want in the future is to pay for outcomes. People want service that is reliable, consistent, and timely, and they want service that is specified to their needs, inputs, and budget. We are on a trajectory where these outcomes will increasingly be produced all, or in part, by software and there is little evidence to suggest that we will be getting off this train any time soon.

I’ve said it before and I’ll say it again. Industries are safe. Services are not. Place your bets and act accordingly. And if you are building in these categories - don’t hesitate to reach out :) Dez [at] firstmark.com

Timely post and well said!

Very interesting. For Vertical AI one of the core factors for growth I see is the strength of the network of founders on their respective verticals. Harvey AI had senior lawyers from the get-go. Without a network it is very hard to sell to lawyers and bankers even if you have an amazing product.