What’s Up Everyone -

Last week, a relatively new startup called Tome raised a $43M series B valuing the business at $300M. According to reporting from Alex Konrad at Forbes, “San Francisco-based Tome passed a million users, 134 days after launch.” That’s an incredible accomplishment to be celebrated. It’s a win for innovation, it’s a win for the founders, and it’s a win for the field of generative AI. On the flip side though, they have made zero dollars. Zilch. Nada. A nice big fat goose egg. As the entire VC market continues to slow, Tome and the broader category of generative AI are the counter-cyclical trend. What’s more, the contrast between Tome’s valuation and it’s monetization to date present us with an interesting question, where exactly are we in the hype cycle of generative AI? What businesses are creating real, genuine, and enduring value? And what businesses are a house of cards, destined to fade into the obscurity of silicon valley history? Using Tome as an example, we can come to a perspective on where we are in the cycle. Let’s dive in.

Now clearly with a million users, and plans to charge customers $10 per month for a monthly subscription, Tome is going to make money. The question is, how quickly? For how long? And how much? Let’s do some super quick math here.

If Tome gets 10% of their current user base to convert into paying users, they’ll be at $12M ARR. If they grow their current user base to a point where they are at 5M paying users, they’re at $600M ARR. $600M ARR is a ton of money.

With $600M ARR, whether it’s the investors or the founders, someone is on their way to owning a sports team (which is sick). But setting aside my own underlying desire to be an NBA team owner, let’s return to our three questions:

How much money could Tome make?

How quickly will Tome make money?

How long will Tome make money for?

Starting with the first of those three questions, we can safely say that Tome has the potential to make a ton of money. Check one for Tome. Now the other two questions are a bit trickier to answer, but I think they’re more important. Speed is a critical aspect of the game in venture. Tome probably has a year or two tops, before it needs to figure out it’s monetization strategy, and it’s overall level of conversion from free to paid users. Personally, as I’ve been trying to figure out where exactly we are in the current hype cycle of generative AI, I’ve found it useful to refer to history as a guide of what to look for when separating signal from noise.

The below chart shows the 5-YR CAGRS of some of the leading technology firms that emerged during the early internet, cloud, mobile technology cycles.

I think these stats are instructive for a few reasons:

They highlight how quickly these businesses found product market fit

They underpin how unique of a moment the commercialization of the internet was

They reinforce the importance of having an investment tailwind that pulls forward demand over a sustained period of time

They illustrate that even during the peak of a hype cycle’s over inflated expectations, valuable companies can be created and will endure

With the exception of Facebook, all of these companies were founded pre-2000 and as a group, they averaged a 400% 5 year CAGR, which is absolutely insane. Now, to be totally fair, is there survivorship bias in these statisitics? 1000%, but the statistics are also evidence that in certain pockets of commercialization, the speed of growth, shouldn’t necessarily be a concern. To drive the point home even further, the below table shows us how quickly it took ChatGPT, TikTok, and Instagram to each reach 100M users

Okay so similarly to Tome’s potential to make a ton of money, clearly using both recent precendents (i.e ChatGPT, TikTok, Instagram) and the historical example of the internet era, Tome has the potential to grow extremely quickly. Check two for Tome.

That leaves us with the final question. How long will Tome make money? I think it’s the hardest question, but also one of the questions that is least asked in these situations. Clearly people are confident that Tome will make money. 1 million people all using your product is a hell of an accomplishment, and it’s not like Tome is going to stand still with where they are at. With all of that fresh VC funding, they are going to be making investments in product, in engineering, and in design. They are going to look to make their models more accurate, more consistent, and more valuable for their consumer. All of these things translate into sales.

However.

Startups have a nasty habit of dying, principally because they’re really freaking hard. Even if you have a million plus users, the Grim Reaper of Silicon Valley is stalking your every move. Even if you are making money today (which as a reminder, Tome isn’t), that does not mean you’re going to be making the kind of money that justifies a $300M valuation tomorrow, or even ten years from now. Startups are about longevity as much as they are about disruption. Companies like HQ Trivia, YikYak, SoundCloud, MySpace, and even Netscape were all disruptive. But did they survive? No! At least not in the sense that they’re public companies throwing off hundreds of millions of dollars of free cash flow every year. At best they get bought on the down swing and sunset by a lagging competitor (ahem, Netscape) at worst they are relegated to the sporadic reminiscence of college friend groups:

“DUDE. Remember when YikYak blew up?” - College Bro #1, now an alumni, 5 years out

“Oh yeah dude, SO BRUTAL. YikYak was ruthless” - College Bro #2, also 5 years out

To drive this point home, let’s look to Netscape as an example. In many ways Netscape was a pioneering company, with pioneering founders. It’s the stuff of Silicon Valley legend, and it literally helped commercialize the internet. Here’s a quote from an old New York Times article describing Mosaic, the web browser Marc Andressen helped initially build while at the University of Illinois and the predecessor to Netscape:

“Available free to Internet users willing to download it to their computers, Mosaic has been acquired by several hundred thousand computer networkers in less than a year, according to several industry estimates. The users include computer scientists, librarians, software developers, magazine publishers, record companies and catalogue distributors, all of whom see it as the first general-purpose navigational tool for the emerging data highway.

So sudden and dramatic has been Mosaic's success in attracting commercial software developers that the program may play a decisive role in determining the shape of the national "information infrastructure" now being debated by Government officials and telecommunications and computer executives.”

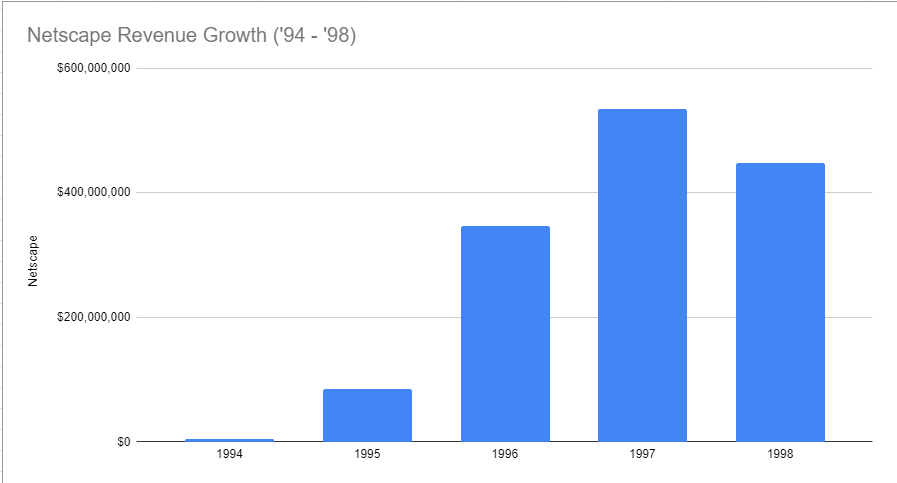

Off the back of his experience building Mosaic, Marky Mark, alongside Jim Clark and with financing from Kleiner Perkins, founded Netscape in early 1994. From 1994 to 1998, Netscape grew from $4M in revenue to ~$450M. Here’s the actual revenue growth during that period

Absolutely astonishing growth, and in 1998 Nestcape was bought for $4.2 billion by AOL. From zero to a $4 billion dollar exit in 5 years?? You love to see it. But as I mentioned earlier, startups have a pesky habit of dying. Netscape isn’t a household name. Netscape isn’t in the same rarefied air as a company like Facebook, or Apple, or Google. So what gives? Notice that decrease from 1997 to 1998? As quickly as Netscape’s ascent began, it’s decline wasn’t far behind.

From 1995 onwards, Netscape went from a peak of ~90% market share to effectively zero by the time AOL decided to end support of Netscape browsers in 2008, formally putting to rest the innovative company that at one point was the default entry point to the internet. Netscape was a victim of intense competition, anti-competitive tactics by Microsoft, and strategic missteps. Here’s an incredible data visualization of what ultimately happened, and Netscape’s Icarian fall. And here’s a chart that tells a similar story:

But Netscape sold for $4B, so why do we care?

Ultimately I think the lesson to learn from Netscape is that even though Netscape was acquired for $4B, in all likelihood it didn’t live up to it’s valuation. The level of competition was too quick and too intense, that it likely wasn’t able to produce the free cash flow over time to justify the initial purchase price. Netscape is a perfect example of a disruptive company not becoming an enduring company. That’s why we care.

So to return to our three questions:

How much money could Tome make?

How quickly will Tome make money?

How long will Tome make money for?

We’ve got a check, check, and an unknown. Tome clearly has the potential to quickly make a TON of money in the next few years, but will it be sustainable? Will Tome be purely a disruptive company? Or an enduring company? Personally, I hope it’s the latter - the founder Keith Peiris seems like an all around good dude, and just someone you want to root for. If companies like Tome succeed, it’s good for the entire ecosystem of venture, and in the long run probably good for the entirety of the US economy.

Okay so with that mini dive on Tome complete, let’s return to my original question, where exactly are we in the hype cycle of generative AI?

With the amount of media attention, trend following, and overall speculation in the space it definitely feels like we’re reaching a peak of inflated expectation. A business like Tome shows us that we are past the technology trigger point, but that we haven’t slogged through the trough of disillusionment. In a lot of ways, it feels like the crypto/web 3 cycle all over again, with the main difference being that more of the generative AI companies being started feel readily applicable, with use cases that boost productivity, and could be explained to a group of totally average people without having to hand wave your way through a bunch of esoteric and poorly named technical terms and ideas. That being said, I’ve heard of some crazy deals getting done, and in all likelihood there are a lot of Generative AI companies that are overvalued, won’t materialize into anything of redeemable value, and will fade into obscurity over time. To take it a step further, for every Tome out there in the world, I’m sure there are dozens if not hundreds of adjacent startups that are less equipped for the opportunity at hand.

Ultimately, I think the more nuanced answer to where we are in the current hype cycle of AI actually centers more around how quickly could we progress through the cycle. The internet has flattened the time it takes for any type of software to be distributed and reach a global scale, and the advent of generative AI and it’s effects could be so disruptive - who’s to say it will operate on any sort of time frame we’ve seen in the past? We may be in a massive period of speculation, but all it takes is one break through, evidenced by the success of ChatGPT, for the technology industry to enter a whole new era of possibility.

All in all, the genie is out of the bottle, generative AI is here to stay, and while the pluraity of companies in the space won’t survive, there will a multiple winners that cross the chasm, and create meaningful outcomes for everyone involved. Ya boy hopefully included :)

If any of the above article/essay resonated with you, drop a comment. I’d love to hear you thoughts. I can also always be reached at dez@firstmarkcap.com. For any ambitious founders thinking about applying AI in the wonderful world of fintech, don’t hesitate to reach out.

Really appreciate you demonstrating the nuanced breakdown of Tome and the general interplay between valuation and monetization when it comes to things like generative AI and other "hype" new technologies and the value of not just a companies TAM - but staying power as well (how long they can make money for) - thanks for this!