Current State of VC

All Things Venture #101

What’s the current state of the VC industry? If you asked a VC how they feel about the market right now, you’d probably hear one of three consistent refrains: You’d hear A) it’s crowded B) it’s highly competitive and C) that returns accrue to the top.

It’s an interesting, consistent commentary especially given the role VCs play in the startup ecosystem. Is VC a dying asset class? Certainly not. Is it facing structural challenges? 100%.

Let’s zoom out a little to investigate why.

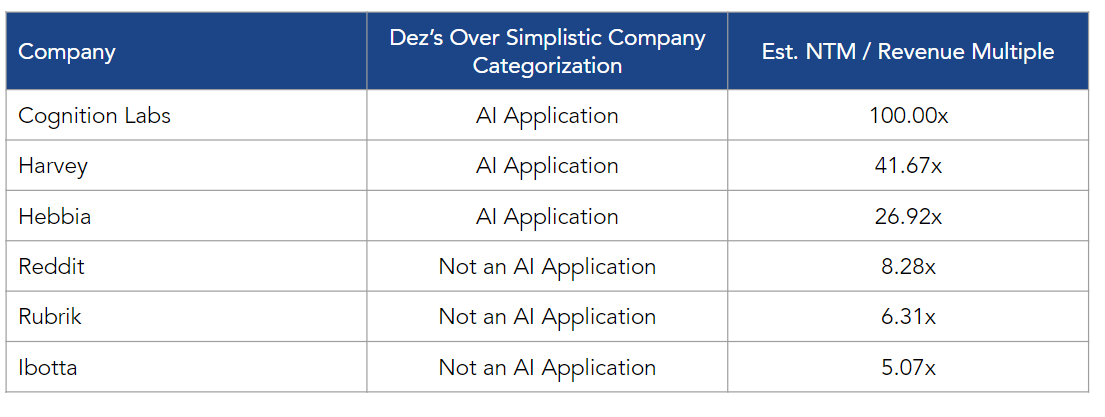

So far in 2024, there have been three high profile VC backed IPOs: Reddit, Rubrik, and Ibotta. As of earlier this week these three companies were respectively worth around $10bn, $6bn, and $2bn of enterprise value and were projected to reach $1.2bn, $922M, and $415M of revenue in the next twelve months.

These are large, well capitalized, well known businesses with thousands to millions of customers/users that love their platforms. These companies have all crossed the proverbial chasm and are now navigating the process of becoming high functioning public companies. These multi-billion dollar outcomes are the stuff of dreams for VCs and quite literally can make our careers 10x over.

However, despite the fact that returning capital is the only thing that matters in the long run for a VC, we (as an industry) somehow remain incredibly willing to suspend disbelief with respect to a core part of our job, pricing.

Over the past few weeks, the early stage startup environment has continued to bifurcate into a tale of two cities (AI native companies, and then everything else).

The AI native companies are focused on the application, inference, and frontier/deep tech model layers. These are businesses like Hebbia which recently raised at a $700M valuation, Cognition Labs which is now valued at $2bn (after 6 months btw, pretty sick), and Harvey which is reportedly close to closing a funding round valuing the company at $1.5bn.

And look, it’s not like we’re living in a funding environment where these valuations are few and far between. They are actually quite common. There are other companies such as Glean (already valued at $2bn), Skild AI (valued at $1.5bn), and Applied Intuition (valued at $6bn) that are reinforcing the trend. I just know that three of these companies in particular, Hebbia, Cognition, and Harvey, have a few things going for them:

They are making money: Hebbia is reportedly at $13M and profitable, Cognition is probably less, maybe around ~$5 - $10M, and Harvey is in the $20M+ range1

They are building a brand & talent density for themselves: If you check any of their employee bases it’s littered with Ivy league grads and tech veterans 2

They have name brand logos as customers: Think PWC, KKR, T-Mobile, Bridgewater, the US Air Force, Centerview Partners, etc.

They are representative of the changing of the guard in application software: Think less workflow, more work product (i.e don’t help me do the work, just do the work for me)

However, dubious unicorn valuations aside, they are all squarely IN the chasm. There is by no means any guarantee that they will survive to see the light of public markets. There is intense competition in the space. The technology they are built on top of could asymptote and not deliver clear enough ROI for their end customers. AND, public company peers are > 20x magnitude of revenue scale, have clearly established themselves as market leaders, and are valued at 5 - 8x forward NTM revenue, not 20 - 100x forward revenue.

Herein lies the structural challenge of VC: There is too much capital, chasing too few assets, which leads to unsustainable markups, which ultimately destroys equity value. BUT nestled within these insane markups, are valuations that in hindsight will look relatively cheap. There are genuine, enduring, generational companies being built today, it’s just that no one can definitively discern which companies will turn out to be Webvan, and which will turn out to be Doordash.

The Doordash’s of the world, in turn then create a windfall of cash for their investors which then kicks off an additional cycle of interest in VC as an asset class. The hamster wheel spins again and in 2040 we’ll just be talking about a new technology du jour to invest behind that will have similarly dislocated pricing. This is the current state of VC. And to elucidate it further, I think there are a few themes about the current state of VC that are incredibly clear:

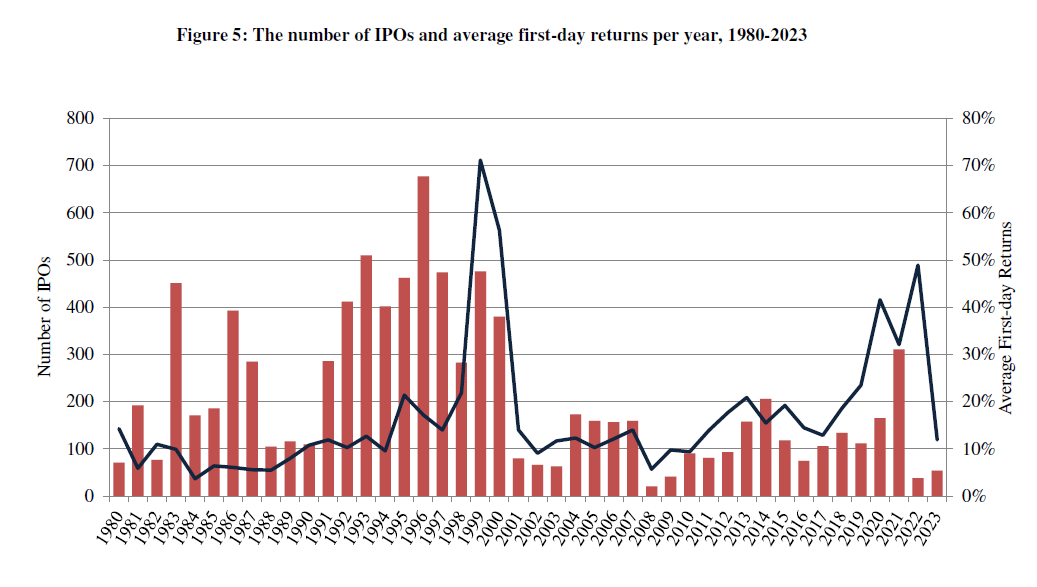

1. We are in a period of low liquidity and somewhere toward the bottom of the market cycle. 2022 was the lowest year on record since the GFC for IPOs and 2023 wasn’t much better.

2. Application software has been the gift that keeps on giving, accounting for 8% of all IPOs since 1996, but it is maturing as a sub-sector of VC investment. Given this, the surface area of TAM opportunities is shrinking

3. VC has never been more competitive. The asset class has grown >4x over the past 20 years. This is the embodiment of, ”Your margin is my opportunity”

4. Price is not a consideration set for perceived n of 1 assets. 100x revenue multiples are accepted and (increasingly) common

If I had to simplify the core thrust of my argument it’d be that when you take $7M and turn it into $4bn, it tends to attract competition, and that competition is the defining factor for the current state of VC. The pricing, the pace of deals, the intensity of deal processes, all of this is downstream of competition, and the competitive dynamics of the VC space today are just thoroughly exposed through the tale of two cities; there’s currently AI native companies and then everything else.

Now the real question to ask ourselves is, if this is where VC is at today, so what? I have my own ideas and strategies I’m putting into play, but I’ll keep them to myself for now. In the meantime, have a great rest of the week everyone and happy hunting.

For the avoidance of doubt, I have not spoken to these companies. These are estimates I’ve gathered from public records & private conversations

For the record I am not saying having either of these a prerequisite for success but they are strong early indicators of aggregating talent density